Jingle bells!

Jingle bells, cash flow swells, profits on the way,

Oh, what fun it is to plan and grow your wealth today!

Jingle bells, balance tells, budgets keep us strong,

Advisers guide through markets wide, all year long!

Dashing through the charts, in a well-diversified sleigh,

Risk is spread apart, compliance lights the way!

Forecasts shining bright, tax savings in our sight,

Planning for the future makes the numbers feel just right!

Ye gads! As we sleigh ride to the end of the year singing traditional Yule tide songs, as above, I am going to make this newsletter cheery if it’s the last thing I do! Because outside of this newsletter you would believe there is very little to cheer!

That’s right, the Budget from the 26th of November seems to have beat everyone into a morass of dismal dreariness and I for one, ain’t having it!

Instead of having a pop at Rachel Reeves (it’s not her fault the country is skint and not enough people know how to earn a quid to get us out of it) we are going to focus on all the good things that have happened that we should be grateful for, because that’s what Christmas is about, right? Let’s focus on what we have rather than what we lack, the people who have our back, rather than the politicians we’d like to sack.

The people we love

Hopefully you’ll be able to get together with your loved ones over Christmas and catch up with old friends. Remember, it may be the last time you’ll have to cope with the side effects of Brussels sprouts and stuffing from one of your relatives. So, although you won’t exactly savour that moment, there may not be many left, so savour the rest of the day. And take photos and videos!

Gifts

Someone taking the time and expense to get you a gift is a massive expression of love! No matter how tight that jumper is, how much you dislike “parfum de Walrus”, or how offended you get from being gifted a ladder / electric sander / circular saw (these may be based on a true story…) they are still a wonderful thing! Except the ladder. I hit my head on that every time I enter the garage. When you’re my size, ladders are largely redundant.

Anyways… financially speaking, this has largely been a good year for you. In January, we will do a roundup of the year. But here are some key things:

You’re still all worried about inheritance tax - but if you’re reading this, you’re not dead, so spend it / gift it / insure it / do something about it.

It’s really easy! But you need to take action… funnily enough, despite contrary opinion, moaning doesn’t actually change anything.

Saying to us “what’s my inheritance tax bill likely to be and how do I reduce it? Whatever you suggest as being best, I will do it!” does actually change something!

If you have done that then you may have made a dent in your inheritance tax bill.

But, that will have been undone by:

Growth in your wealth due to stock market returns:

Year to date (27th Nov 2025) our most popular portfolios have risen by:

In real terms, after cost of living rises which ultimately is all that matters when investing – maintaining the value of your money, if you are a client of ours in Power Factor 80% then you are up 7.48%. Which is totally awesome! And if that isn’t enough to delight you then your Christmas cards from us are going in the post in the next few days…

What is the message here? Well, I don’t know, I don’t write to structure, there’s enough of that in my day job, this is freestyle baby! But what I do know is that even if all seems dour and dismal around you and taxes are rising, then global stock markets have come to the rescue (again!) to cover that off.

As a business owner, I need to control risk. There is some risk I can control and some I can’t. The risk I can’t control I don’t worry about. Because what’s the point? One of those is what tax changes a government can or can’t make in the future.

As a child, my favourite toy was Action Man and consequently, I run my business like a military operation run by toy soldiers! Action Man taught me about the ‘Pincer Movement’. On the one side I have controls in place that ensure our regulator, the Police, HMRC etc never have to knock on our door! Or bash it down for that matter. These are top-down controls of oversight, compliance and process, with external independent auditors reviewing them annually. The other side of the pincer, a culture of doing the absolute best things for our clients every time. One and only rule: if it most likely benefits the individual client - we do it.

If one side of the pincer fails, the other will endure.

Our ‘pincer’ for the current down beat mood in the UK is this:

We can’t control external factors, global geopolitics, Budgets, the mood on the news etc.

But we can control what we do with our own finances, and we can maximise them whatever happens. The chat we have at the pub should be about fun times and great gags, not what brings us down.

These are (almost) certainties to cling on to:

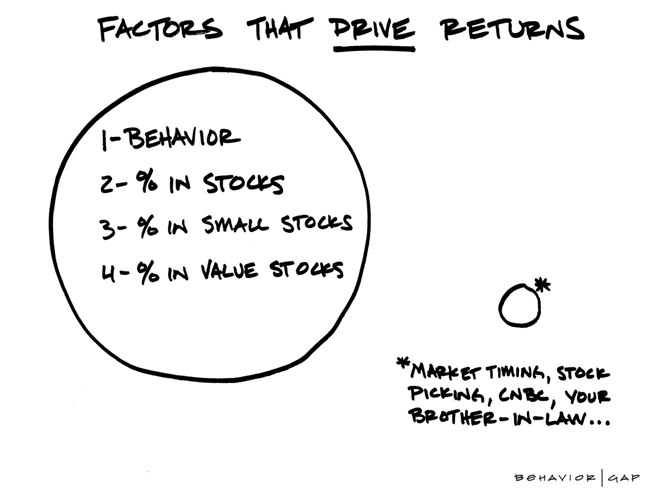

• Equities (shares) earn more than other mainstream assets

• The proportion of your portfolio you have in equities determines circa 90% of your return.

• Costs of investment are then a determinant – our portfolios are 1.2% compared to profession average of 1.89% (Next Wealth FABB report 2024)

• The amount of money you have in Small and Value companies is another determinant (this is in our Power Factor and Green portfolios above, not the ‘Tracker’ ones)

If you’re not bothered about how your money has gone up in value (this is good! Rises and falls - you should treat those two imposters just the same), your behaviour is the ultimate determinant of how much you will earn:

Stay invested – only withdraw to spend. That is the only reason to withdraw! Anything else, like news, or some TikTok video is you guessing and most of the time, is making a mistake.

You have a plan – stick to it, financially! Except, if life presents a ‘life’ opportunity to have more fun, etc then we can look at how to adapt it.

Key things from the Budget

I have mentioned here the key things I think will affect the majority of our clients, not necessarily those that have received most headlines.

Dividend Rate Increases

The Basic rate and Higher rate will increase by 2% going from 8.75% to 10.75% and 33.75% to 35.75%. The additional rate has remained the same at 39.35%.

This will most likely affect business owners that pay themselves via dividends and those with large amounts of money invested in ‘General Investment Accounts’ (GIA).

This makes use of ISA allowances all the more critical, and anyone investing in a cash ISA when they have money in a GIA is losing out on saving more tax, as the investment would be in an asset more likely to earn more money than a bank account, and therefore the tax saving is greater.

Rental Income

Rent from Buy to Let properties will also be taxed at 2% more so 22%, 42% and 47%. This applies from April 2027…. I keep on about this, but rental properties are not a good investment:

• Property does not, on average, earn as much as equities

• The tax rates are higher anyway, and getting even more so

• They are illiquid – you need to sell them to get money out and this makes it difficult to live a life!

• They are a job – maintenance, accounts, dealing with agents. That’s a job not an investment. Any value you add through building or your interior design skills is also a job and shouldn’t be classed as investment returns.

Pensions

No change. No change to tax free lump sum allowance. Stop believing the headlines of the rumour mill! Believe in Steve!

VCT

Venture Capital Trusts – The tax relief on these is reducing from 30% to 20% of the amount invested from April 2026. So, if you want to benefit from 30% tax refund then now is the time to invest more.

Salary Sacrifice

This is primarily used for pension payments and means the employer saves 15% in National Insurance and the employee at their highest rate. This is being capped at £2,000 from April 2029. This will affect anyone earning more than £40,000 and sacrificing 5% of their salary into a pension, and businesses too in the extra expenses of funding pension contributions.

Key people affected:

Business Owners, this is a budget that has not been good for you! Higher National Insurance due to loss of Salary Sacrifice on top of the higher rate from last budget, the loss of VCT relief if you are using that as a strategy to make withdrawals from your business, higher dividend tax rates and also, if you are planning to convert to Employee Ownership Trust, the tax relief on that has been halved too.

Those that have retired, will be largely unaffected unless you have a lot in GIA’s. Employees will also be affected by the Salary Sacrifice cap from 2029… but at least that’s a while away.

All in all, if you’re a client with us, then I would say that 2025 has been a great year for you. Assuming you are on that train, here’s some good things about us, that you can talk about too!

Juggling Mind and Money Podcast – Budget Special – on Thursday 4th December

Tune into us and listen to Luke James and I chat about the Budget. If you’ve not listened before, tune in to others too! Check out all episodes here!

New Model Adviser - Top 100

We have been named as one of the top 100 advice firms in the UK. Good eh? I have to say, I only entered because Stevie B (long time - 15 year client) said he’d met another adviser whose firm was in it and was impressed. So I said I’d get us in there and I did. Very easy. To paraphrase Brian Clough, I wouldn’t say we were the best financial planning company in the UK, but we are in the Top One 😊 at the very least for photo they used!

Fond Farewells and Excitable Hellos!

One of us is leaving! In fact posting this will be one of her last tasks! Stacey is off to set up a recruitment company with her boyfriend and smash business ownership. Good luck Stace! We will miss you. Also, it’s the first time we have not had a Weatherstone with us for well over 10 years, which is a loss of stability that we will miss.

New starters

We have a new advisr and two people in the engine room starting in December/January. We are super excited to add these talented people to our group! More about them later, one starts this morning and probably not a good look to make her have a photo done on the first day.

New Portal / Communication tool

We are getting more high tech! In the new year we will be launching an App for your phone. So you can look at your full portfolio, secure message us, sign some documents, all through our portal. You are also able to connect your other accounts that are not managed to us, to it. Don’t worry, it’s all secure, but this means you will have less work to do in telling us your numbers as we would be able to see them directly. This means more efficient, secure and accurate financial planning for you.

Merry Christmas

Listen, who knows what the future holds, but I for one hope and expect it will be great! There will be dips along the way but largely it will be better than it has been. That is the so far endless arc of human progress. I don’t see why it would change.

So, with that, have a great Christmas and resolve to spend more of your money doing the things you love and paying other to do the things you dislike!

Have a great time and see you in 2026

Disclaimer: This article does not constitute financial advice. We recommend that you speak to a qualified financial planner for advice tailored to your individual circumstances and goals. Financial markets may go up or down, and you are not guaranteed a return on your investment. Past performance is not necessarily a guide to future performance. Financial details including benefits to the treatment of tax will depend on your individual circumstances and, while checked at the time of publication, may be subject to change in future.

*When clicking a link to an external website, Lucent Financial Planning Ltd cannot be held responsible for the content of the external website.

.jpg)

.jpg)